Why It’s Best NOT To Pay Off Your House

Oh to be debt free…

The dream of millions of Americans. That sweet, sweet moment you can someday make your last loan payment, sit back and relish in the fact that you no longer owe the bank a cent of interest. It’s a noble pursuit, but is it really what you should be doing to build long-term wealth?

The short answer is a resounding no.

But this is where we must reexamine our fundamental understanding and relationship with debt, and how we think of it. Let’s start with a brief review of exactly what debt is.

Debt

noun a sum of money owed.

2 the state of owing money.

3 a feeling of gratitude for a favour or service.

-Oxford English Dictionary

I like to distill it to the idea of “renting” money. Its concept was inevitable and necessary, dating back to as early as 3500BC when merchants in Mesopotamia inscribed clay tablets with a borrower’s seal, creating the promissory note.

As civilization grew and currency evolved from cows to cowrie shells, “cash” in any form was simply not enough to embark on the world’s most ambitious endeavors. The ability to “rent” money in order to buy assets that would in turn earn money allowed for far more efficient use of resources and an explosion in productivity.

Picture this. If you had 100 cowrie shells with which you could buy tea, travel and sell at a 100% profit for 200 cowrie shells… would it not make more sense to take out a 900 shell loan at 10% interest and buy 1000 shells of tea to sell for 2000? In this case, instead of a 100 shell profit, you could earn a 1010 shell profit. (2000 in sales minus 990; 900 loan principal plus 10% interest). There’s also the added economy of scale. The hypothetical trip to the far away tea market likely costs very much the same whether you’re packing 10kg or 100kg of tea. The debt instrument also provides an incredible opportunity for the person on the other side of the table. They’re able to put their idle cash to work and make a 10% return. A true win-win.

The day that money was freed to go make more money was the day it was truly born in its current state.

So how does any of this relate to my home loan? Well now that we have a better understanding of how money wants to work, we can explore further.

Let’s look at a tale of two twin brothers. We’ll call them Jake and Chris.

Jake and Chris are both 30 years old. Both work in steady jobs that pay $60,000/yr or $5,000/mo. Let’s say this is after-tax for simplicity.

On January 1 2020 they both buy houses for $300,000, putting 20% or $60,000 down and getting 30 year fixed rate mortgages at 4% interest. The monthly payment including property taxes and home owners insurance comes to $1,300/mo leaving them with $3,700/mo to pay for the rest of life’s expenses.

Jake despises debt. He recognizes that over the course of 30 years, his total payments to the bank will end up being $412,448 on a $240,000 loan. That’s $172,485 in interest the bank will make off of him! Jake can’t stand this and wants to be debt free so he decides to pay an additional 1000/mo in order to accelerate his payoff. He calculates that this will allow him to pay off his mortgage in just 12 years and save a ton of money on interest to the bank. Instead of paying $172,485 in interest over 30 years, he’ll now only pay $62,598 over 12.

Chris on the other hand, understands the benefits of good debt and how to use it over time to build wealth. Instead of using that $1000 every month to pay down his mortgage, he puts it into a brokerage account and invests it knowing the stock market returns 7-9% per year over the long term. Or even better- in real estate syndications which return monthly cash distributions, high-teens returns and even more tax benefits.

5 years later, let’s take a look at how the two brothers compare.

Jake has paid his mortgage down to $132,780 but has almost nothing in savings. Chris’ mortgage balance is much higher at $211,470 since he’s solely been making the minimum payment of $1300/mo. Jake has significantly more home equity now… $78,690 more.

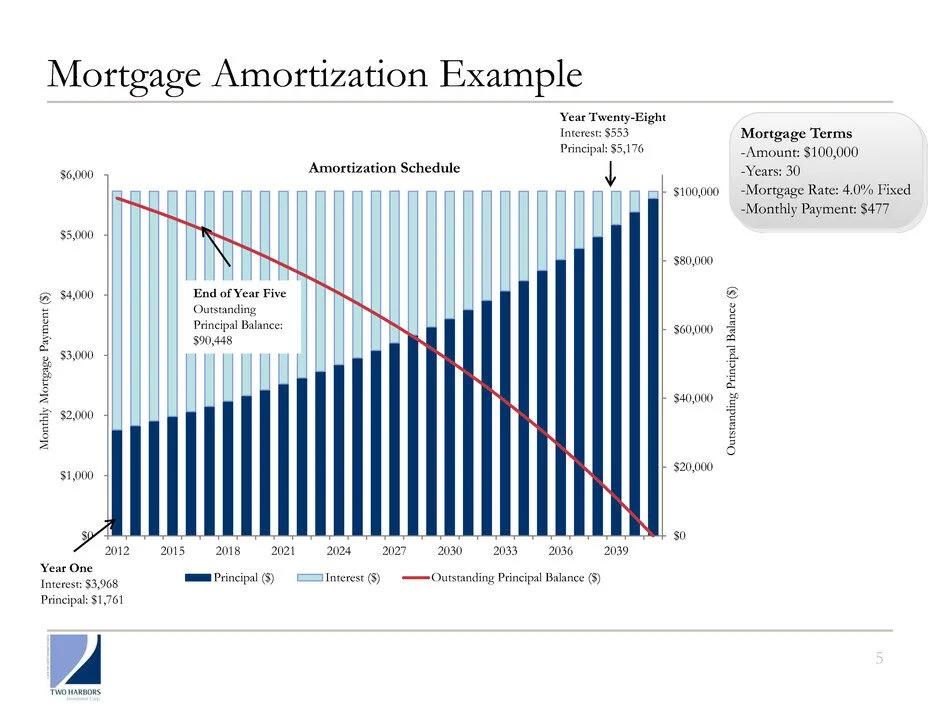

Since Chris has been investing that $1000 in the S&P 500, or passive real estate deals from the same time, how’s he fairing? Assuming an 8% return, his brokerage account now has $75,500. From purchase until now, Jake has had the upper hand. This is because paying down your mortgage in the early years has more significant impact due to the amortization schedule (the amount each month that goes to principal vs interest which reverses during the lifetime of the loan).

See below.

https://www.sec.gov/Archives/edgar/data/1465740/000146574012000062/a09122012primeronagencyp.htm

Now let’s compare how they’re doing in year 7. Just two years later.

Jake’s mortgage balance is down to $111,962 while Chris’ is $206,085. Jake has $94,123 more in home equity, but Chris’ brokerage account balance is $114,600. Chris has definitively taken the lead.

Here’s the kicker though. Let’s say they both simultaneously lose their jobs… While Jake does have a lot of equity in his home, he can’t access it without selling because now that he doesn’t have a job he can’t get a loan. He also doesn’t have enough in savings to float his expenses or service his mortgage payment. Jake’s in a bind. At this point he may think to call the bank and explain that he’s been making early payments all these years, maybe he could slide on a few payments since he’s on hard times now? Unfortunately he’ll be informed that no matter how much you prepay, next month’s payment is always due— on time and in full.

If he can’t find a way to continue paying his $1300/mo loan, in 90 days the bank will begin the foreclosure process, ultimately taking his house, demolishing his credit and leaving him with nothing. He’ll be forced to fire sale it at a discount in order to avoid foreclosure.

Chris on the other hand now has $114,600 in his brokerage account. He liquidates $20,000 in stock, puts his mortgage on auto pay and takes a vacation to the Caribbean before returning home a few weeks later to leisurely resume his job search.

Maybe paying down that mortgage wasn’t so smart after all…

But let’s forget about that unfortunate scenario for a moment and go a little further down the road assuming they never lost their jobs. To exactly 12 years from purchase when Jake finally pays off his house and is debt free!!

Seeing as 12 years have past, the properties have surely appreciated in value. The properties they both bought for $300,000 are now worth $485,000 (a modest 4% per year). Jake owns his house free and clear, so he now has zero payments and the full $485,000 in equity. Chris still owes $176,778 to the bank and continues his dutiful $1300/mo payments. His house is worth the same $485,000 and he has $308,222 in equity. But he also has $244,731 in his brokerage account. His account balance plus his home equity puts him at $552,953. His brokerage account will continue to compound at an average 8% clip, and he’ll enjoy the continued tax deductions associated with his mortgage interest for the next 18 years. Not to mention the safety that comes with having liquid assets available for a rainy day.

To take it a step further, if Chris bought rental property with some of his savings rather than investing all of it in the brokerage account, he could have accelerated his wealth building even more by using additional leverage to control larger amounts of real estate. Through rental property investing, he could have achieved healthy double digit cash-on-cash returns and his property portfolio would not only grow through appreciation and cashflow like his stock portfolio (price appreciation and dividends) but also through principal pay down and tax benefits.

This not to say all debt is good debt. High interest credit cards are poison to personal finance. And if Chris spent his extra $1000 per month on frivolous things rather than socking it away in that brokerage account, he’d end up much poorer compared to his brother. Obviously, if the choice is between spending it or paying down debt with it, absolutely pay down the debt. But one must realize that debt is a powerful tool when understood and used properly.

Debt is an instrument without which our modern world would not exist. In its absence there could not be skyscrapers, airliners, cell networks, automobiles or worldwide shipping lines… The list is endless.

So now that you see the light, you can easily see that you should not seek not to eliminate debt, but to use it intelligently in your wealth building journey through life.

But hey, don’t take my word for it. Run your own calculations by using tools such as these to make better financial decisions:

https://www.nerdwallet.com/banking/calculator/compound-interest-calculator

Turbine Capital specializes in commercial real estate syndication deals for pilots and other high-income w2 professionals. If you’d like to learn more about commercial real estate investing, please join our investor club.